Five Institutional Trends Dominated in 2H 2023

Natixis Investment Managers Solutions portfolio consultants monitor asset classes, investment products, and market activity both in real time and from a historical perspective. Compelling institutional trends are summarized below.

1. E&Fs Lead Crowded Performance Pack. Strong equity market performance helped institutional investment programs recover a portion of 2022 losses. Endowments and Foundations returns outpaced other plan types through Q3 2023.

Percentile Rank – YTD Performance Through Q3 2023

Source: Natixis Investment Managers Solutions, InvMetrics

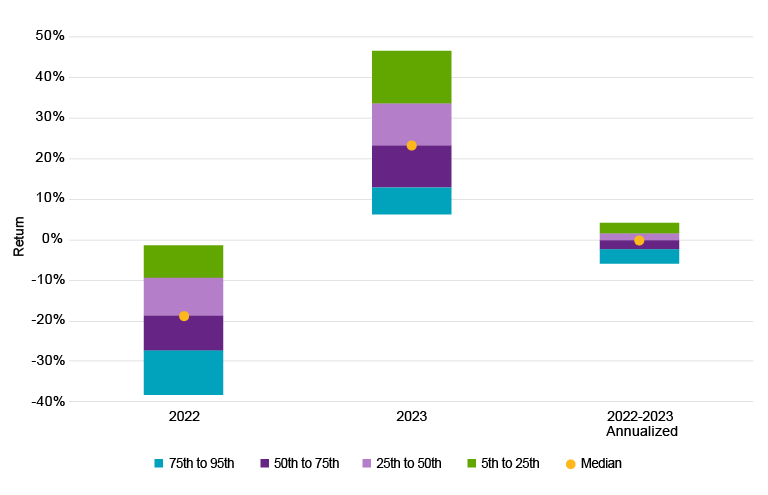

US Large Equity Performance by Percentile

Source: Morningstar, Natixis Investment Managers Solutions

Natixis 2024 Institutional Outlook

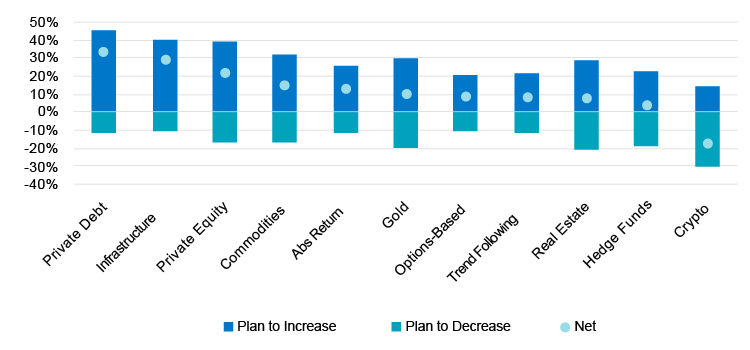

Plans to Increase/Decrease Allocations, Alts Categories

Source: Natixis Institutional Outlook 2024, eVestment

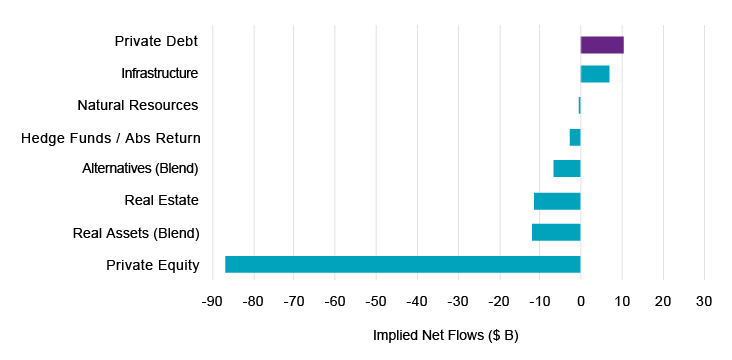

Required Flows to Match Asset Allocation Policy (6/30/23 Est.)

Source: Natixis Institutional Outlook 2024, eVestment

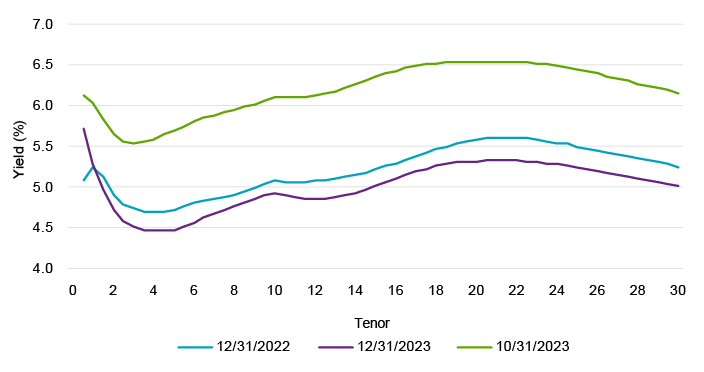

FTSE Above Medium Yield Curve

Source: FTSE, Bloomberg

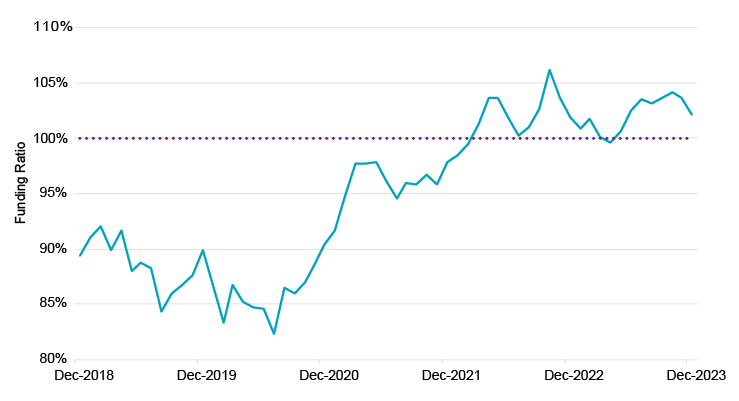

Milliman 100 Pension Funding Index (12/31/18–12/31/23)

Source: FTSE, Bloomberg

Institutional Investing Trends

Summary of Endowments & Foundations' leading performance, private debt's soaring popularity, and other top institutional portfolio trends.

Download PDF

Learn More

Interested to see how institutions’ funded status and asset levels will respond to 2024 market conditions?

Contact Us

Natixis Investment Managers, Global Survey of Institutional Investors conducted by CoreData Research in October and November 2023. Survey included 500 institutional investors in 27 countries throughout North America, Latin America, the United Kingdom, Continental Europe, Asia and the Middle East.

The S&P 500® Index is a widely recognized measure of US stock market performance. It is an unmanaged index of 500 common stocks chosen for market size, liquidity, and industry group representation, among other factors. It also measures the performance of the large-cap segment of the US equities market.

This content is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the author only and do not necessarily reflect the views of Natixis Investment Managers, or any of its affiliates. There can be no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis does not represent the actual or expected future performance of any investment product. We believe the information, including that obtained from outside resources, to be correct, but we cannot guarantee its accuracy. The information is subject to change at any time without notice.

The data contained herein is the result of analysis conducted by the Natixis Investment Managers Solutions consulting team on model portfolios submitted by Investment Professionals. The Moderate Peer Group consists of model portfolios that have been analyzed by the consulting team and have been designated as moderate by Investment Professionals.

Natixis Investment Managers Solutions collects portfolio data and aggregates that data in accordance with the peer group portfolio category that is assigned to an individual portfolio by the Investment Professionals. At such time that a Professional requests a report, the Professional will categorize the portfolios as a portfolio belonging to one of the following categories: Aggressive, Moderately Aggressive, Moderate, Moderately Conservative, or Conservative. The categorization of individual portfolios is not determined by Natixis Investment Managers Solutions as its role is solely as an aggregator of the pre-categorized portfolios. Please note that risk attributes of the Moderate Peer Group will change over time due to movements in the capital markets. Portfolio allocations provided to Natixis Investment Managers Solutions are static in nature and subsequent changes in a Professional’s portfolio allocations may not be reflected in the current Moderate Peer Group data.

Investing involves risk, including the risk of loss. Investment risk exists with equity, fixed income, international and emerging markets. Additionally, alternative investments, including managed futures, can involve a higher degree of risk and may not be suitable for all investors. There is no assurance that any investment will meet its performance objectives or that losses will be avoided.

This document may contain references to copyrights, indexes and trademarks that may not be registered in all jurisdictions. Third-party registrations are the property of their respective owners and are not affiliated with Natixis Investment Managers or any of its related or affiliated companies (collectively “Natixis”). Such third-party owners do not sponsor, endorse or participate in the provision of any Natixis services, funds or other financial products.

Index information contained herein is derived from third parties and is provided on an “as is” basis. The user of this information assumes the entire risk of use of this information. Each of the third-party entities involved in compiling, computing or creating index information disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to such information.

CFA® and Chartered Financial Analyst® are registered trademarks owned by the CFA Institute.

6211306.1.1