5 Ways to Prepare Your Bond Portfolio for a Recession

Federal Reserve (Fed) interest rate hikes and rising inflation continue to roil fixed income markets – and now we’re hearing more about the possibility of a recession. Here are five ideas to help recession-proof your fixed income portfolio, drawing on data from the Global Financial Crisis (GFC) and Covid recessions.

Please keep in mind that these ideas are suggestions and may not be appropriate for all investors. And there is no guarantee that the ideas presented will result in gains or prevent losses.

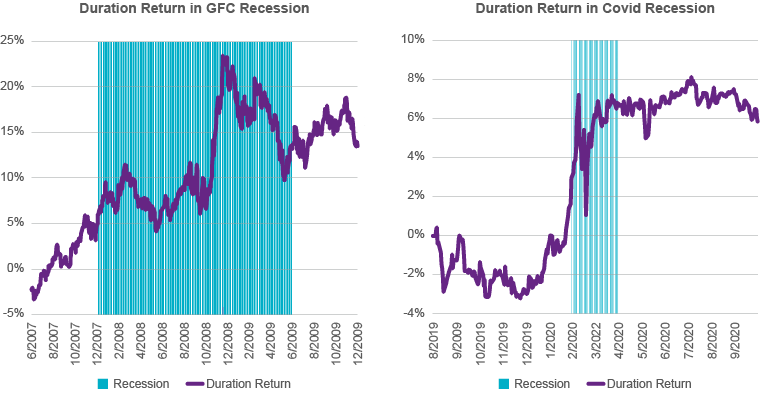

#1 – Extend Duration

While this strategy didn’t work throughout most of 2022 as interest rates rose rapidly, there is now a new starting point for Treasury yields. The Fed has hiked rates in March, May, June, July, and September – a total of three percentage points – and the market has priced in additional hikes for November, December and even into early 2023. Now we have plenty of room for yields to fall. Continued recessionary pressure would have investors start pricing in an earlier pause if not a pivot in 2023. This could mean lower rates and a meaningfully positive return for duration exposure.

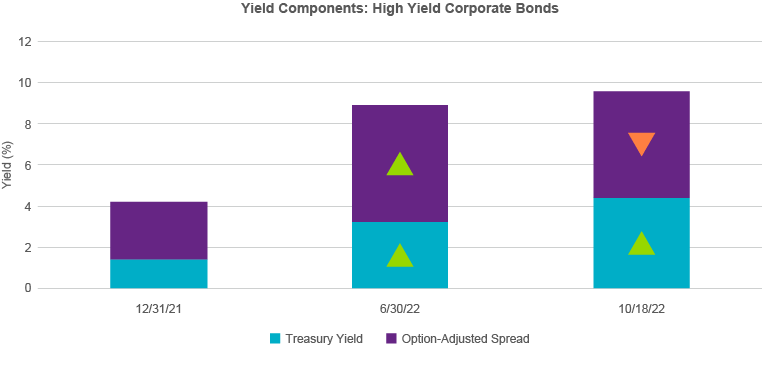

High yield corporates and bank loans provide extremely attractive yields, but the recent yield increases have been almost entirely Treasury-driven. Credit spreads have been remarkably well behaved even as equities have sold off. A ramp up in recessionary fears could push spreads higher and wipe away your yield advantage in these riskier segments of fixed income. But holding a portion of your portfolio in return-seeking fixed income is still reasonable. In the Global Financial Crisis, high yield spreads peaked months before equities bottomed, and credit outperformed during the second half of the recession and into the recovery. A similar dynamic would say be cautious initially, but be prepared for a sharp rally during the recovery period. And given that the timing will be difficult to predict, don’t slash all return-seeking fixed income. But you may want to repurpose outsized allocations to high yield, bank loans and emerging market fixed income to increase quality and better insulate your portfolio for the onset of recession.

The dollar’s reputation as a safe haven currency is born out of outperformance in the depths of past recessions. Non-USD developed market fixed income, which likely has lower yields than US Treasuries and which derives the majority of its volatility from currency movement, does not serve a meaningful role for a US investor trying to recession-proof a fixed income portfolio.

Liquidity can become strained in a recession, particularly a disruptive recession. Even US Treasuries, often considered the most liquid fixed income security, ran into liquidity issues during the height of Covid-related volatility in March 2020. Investors with known liquidity needs could consider a small cash allocation to avoid being a forced seller in a liquidity crunch. But to the extent possible, try to be patient. Past recessions are typically not well aligned with fixed income drawdown periods, and investors shouldn’t confuse short-term volatility with long-term risk of loss. Duration – while volatile – should help provide positive returns in the first half of the recession. Spreads – while susceptible to short-term losses – often balance out in the late recession and recovery period and erase any short-term losses.

Both of the past two recessions saw fixed income volatility spike. The MOVE index, which measures volatility in the US Treasury market, shows we’re already at elevated volatility levels in 2022, presumably before a recession has even begun. Think of active management as an insurance premium. You pay a management fee across often quiet markets for an active bond manager’s expert navigation of a recession’s choppier waters.

The 2022 fixed income market continues to provide challenges, but that shouldn’t stop you from a few portfolio tweaks to better prepare for a recession. Adding duration, increasing quality, avoiding currency, staying patient, and leaning on active management is a recipe for a more recession-proof bond portfolio for you and your clients.

This content is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the author only and do not necessarily reflect the views of Natixis Investment Managers, or any of its affiliates. There can be no assurance that developments will transpire as forecasted, and actual results will be different. Data and analysis do not represent the actual or expected future performance of any investment product. We believe the information, including that obtained from outside resources, to be correct, but we cannot guarantee its accuracy. The information is subject to change at any time without notice.

The data contained herein is the result of analysis conducted by Natixis Investment Managers Solutions’ consulting team on model portfolios submitted by Investment Professionals.

Natixis Investment Managers Solutions collects portfolio data and aggregates that data in accordance with the peer group portfolio category that is assigned to an individual portfolio by the Investment Professionals. At such time that a Professional requests a report, the Professional will categorize the portfolios as a portfolio belonging to one of the following categories: Aggressive, Moderately Aggressive, Moderate, Moderately Conservative, or Conservative.

The categorization of individual portfolios is not determined by Natixis Investment Managers Solutions, as its role is solely as an aggregator of the pre-risk attributes of the Moderate Peer Group and will change over time due to movements in the capital markets.

Portfolio allocations provided to Natixis Investment Managers Solutions are static in nature, and subsequent changes in a Professional’s portfolio allocations may not be reflected in the current Moderate Peer Group data. Investing involves risk, including the risk of loss. Investment risk exists with equity, fixed income, international and emerging markets. Additionally, alternative investments, including managed futures, can involve a higher degree of risk and may not be suitable for all investors. There is no assurance that any investment will meet its performance objectives or that losses will be avoided.

Please keep in mind that these ideas are suggestions and may not be appropriate for all investors. And there is no guarantee that the ideas presented will result in gains or prevent losses.

#1 – Extend Duration

While this strategy didn’t work throughout most of 2022 as interest rates rose rapidly, there is now a new starting point for Treasury yields. The Fed has hiked rates in March, May, June, July, and September – a total of three percentage points – and the market has priced in additional hikes for November, December and even into early 2023. Now we have plenty of room for yields to fall. Continued recessionary pressure would have investors start pricing in an earlier pause if not a pivot in 2023. This could mean lower rates and a meaningfully positive return for duration exposure.

Source: Natixis IM Solutions, Factset. Duration return defined as the cumulative return of Bloomberg 7–10 year Treasury Index, less the Bloomberg Short Treasury Index, beginning 6 months before the start of a recession and ending 6 months after the end of the recession.

High yield corporates and bank loans provide extremely attractive yields, but the recent yield increases have been almost entirely Treasury-driven. Credit spreads have been remarkably well behaved even as equities have sold off. A ramp up in recessionary fears could push spreads higher and wipe away your yield advantage in these riskier segments of fixed income. But holding a portion of your portfolio in return-seeking fixed income is still reasonable. In the Global Financial Crisis, high yield spreads peaked months before equities bottomed, and credit outperformed during the second half of the recession and into the recovery. A similar dynamic would say be cautious initially, but be prepared for a sharp rally during the recovery period. And given that the timing will be difficult to predict, don’t slash all return-seeking fixed income. But you may want to repurpose outsized allocations to high yield, bank loans and emerging market fixed income to increase quality and better insulate your portfolio for the onset of recession.

Source: Factset

The dollar’s reputation as a safe haven currency is born out of outperformance in the depths of past recessions. Non-USD developed market fixed income, which likely has lower yields than US Treasuries and which derives the majority of its volatility from currency movement, does not serve a meaningful role for a US investor trying to recession-proof a fixed income portfolio.

Source: St. Louis Fed

Liquidity can become strained in a recession, particularly a disruptive recession. Even US Treasuries, often considered the most liquid fixed income security, ran into liquidity issues during the height of Covid-related volatility in March 2020. Investors with known liquidity needs could consider a small cash allocation to avoid being a forced seller in a liquidity crunch. But to the extent possible, try to be patient. Past recessions are typically not well aligned with fixed income drawdown periods, and investors shouldn’t confuse short-term volatility with long-term risk of loss. Duration – while volatile – should help provide positive returns in the first half of the recession. Spreads – while susceptible to short-term losses – often balance out in the late recession and recovery period and erase any short-term losses.

Source: FactSet

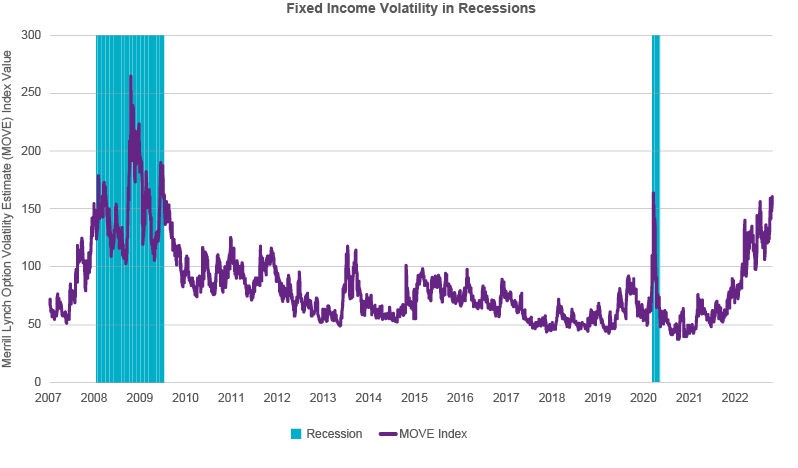

Both of the past two recessions saw fixed income volatility spike. The MOVE index, which measures volatility in the US Treasury market, shows we’re already at elevated volatility levels in 2022, presumably before a recession has even begun. Think of active management as an insurance premium. You pay a management fee across often quiet markets for an active bond manager’s expert navigation of a recession’s choppier waters.

Source: Bloomberg, ICE BofAML MOVE Index

The 2022 fixed income market continues to provide challenges, but that shouldn’t stop you from a few portfolio tweaks to better prepare for a recession. Adding duration, increasing quality, avoiding currency, staying patient, and leaning on active management is a recipe for a more recession-proof bond portfolio for you and your clients.

The data contained herein is the result of analysis conducted by Natixis Investment Managers Solutions’ consulting team on model portfolios submitted by Investment Professionals.

Natixis Investment Managers Solutions collects portfolio data and aggregates that data in accordance with the peer group portfolio category that is assigned to an individual portfolio by the Investment Professionals. At such time that a Professional requests a report, the Professional will categorize the portfolios as a portfolio belonging to one of the following categories: Aggressive, Moderately Aggressive, Moderate, Moderately Conservative, or Conservative.

The categorization of individual portfolios is not determined by Natixis Investment Managers Solutions, as its role is solely as an aggregator of the pre-risk attributes of the Moderate Peer Group and will change over time due to movements in the capital markets.

Portfolio allocations provided to Natixis Investment Managers Solutions are static in nature, and subsequent changes in a Professional’s portfolio allocations may not be reflected in the current Moderate Peer Group data. Investing involves risk, including the risk of loss. Investment risk exists with equity, fixed income, international and emerging markets. Additionally, alternative investments, including managed futures, can involve a higher degree of risk and may not be suitable for all investors. There is no assurance that any investment will meet its performance objectives or that losses will be avoided.

5053627.1.1